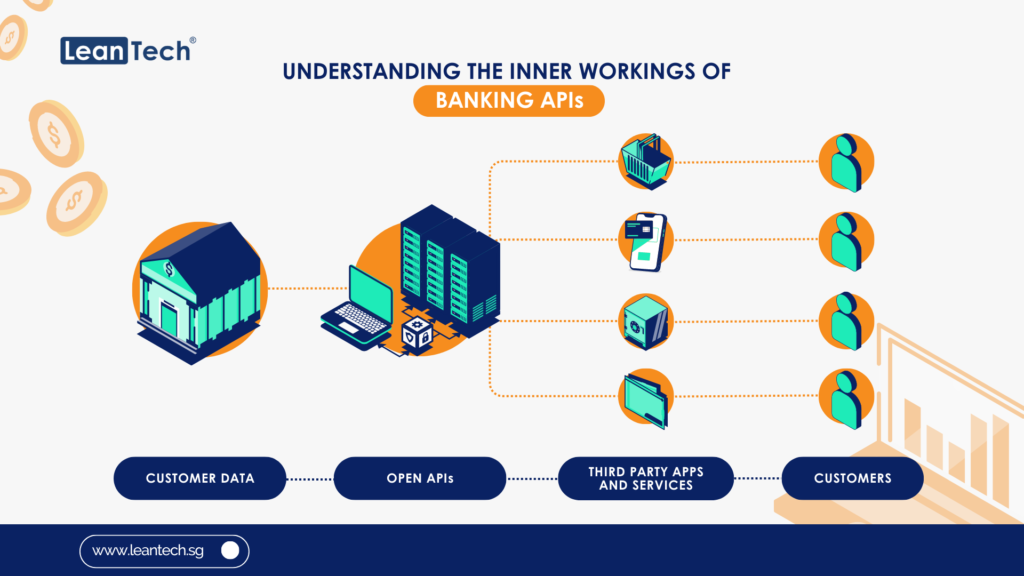

In the modern financial ecosystem, there is a growing emphasis on data sharing and collaboration among various stakeholders. This shift is driven by open banking frameworks, where data sharing in financial services serves as a cornerstone for innovation. The landscape involves a diverse array of participants, including banks, fintech companies, regulators, consumers, and technology providers. Each group plays a vital role in enhancing competition, fostering innovation, and increasing consumer choice.

The Role of Banks in Open Banking

-

Transitioning from custodians of customer data to facilitators of open banking.

-

Complying with regulatory mandates like the European Union’s PSD2, which requires customer-permissioned data sharing.

-

Embracing open banking initiatives to enhance service offerings and maintain customer loyalty.

A report from the Bank for International Settlements highlights that many jurisdictions are adopting frameworks to encourage or mandate data sharing in financial services.

Fintech Companies: Innovators in the Ecosystem

-

Accessing bank data through APIs to develop tailored financial products.

-

Prioritising cybersecurity and transparency to build consumer trust.

-

Addressing data privacy concerns, as 79% of respondents in a Deloitte survey expressed concerns about data sharing.

The Crucial Role of Regulators

-

Establishing guidelines for data sharing practices.

-

Approaches vary, with some regions adopting prescriptive regulations and others favouring market-driven initiatives.

-

Encouraging competition, as noted by the Worldline report:

“PSD2 has created a competitive environment for payment services across Europe.”

Consumer Perspectives: Their Role in Data Sharing

-

Empowering the ecosystem by granting permission for the use of their financial data.

-

Driving innovation by enabling personalised financial services, such as tailored loans, investment advice, and budgeting tools.

-

Benefiting from enhanced financial offerings, including lower fees, better rates, and improved service convenience.

-

Addressing concerns: While consumers are willing to share data for better services, security and privacy remain key considerations. Building trust through transparency and secure data handling is critical to encouraging their participation.

Approximately 60% of consumers prefer sharing significant information with reputable institutions for lower price.

The Role of Technology Providers in Open Banking

-

Supplying the infrastructure for secure data exchange.

-

Mitigating risks such as data breaches.

-

Driving growth, as the open banking market is projected to grow to $43 billion by 2026.

-

Enabling seamless collaboration through API standardisation and enhanced cybersecurity solutions.

The way forward

The future of open banking and open finance relies on collaboration among banks, fintech companies, regulators, consumers, and technology providers. By addressing challenges like regulatory compliance, data security, and consumer trust, these stakeholders can create a more inclusive and efficient financial ecosystem. Collaboration and innovation remain critical as the industry evolves in an increasingly digital world.

Join the conversation on how open banking is transforming finance. Share your thoughts below or contact us to learn more about how these changes may impact your business.

Summary of Key Points

What are the key enablers of FinTech? Artificial intelligence, blockchain, cloud computing, IoT, open-source technologies, and regulatory support drive FinTech innovation and growth

What does open banking enable? Open banking enables secure data sharing between banks and third-party providers, fostering innovation, competition, and personalised financial services

What are the key pillars of open banking? Control, security, uniformity of conditions, insurance, monetisability of APIs, and open banking inclusion are essential for a functional open banking ecosystem.

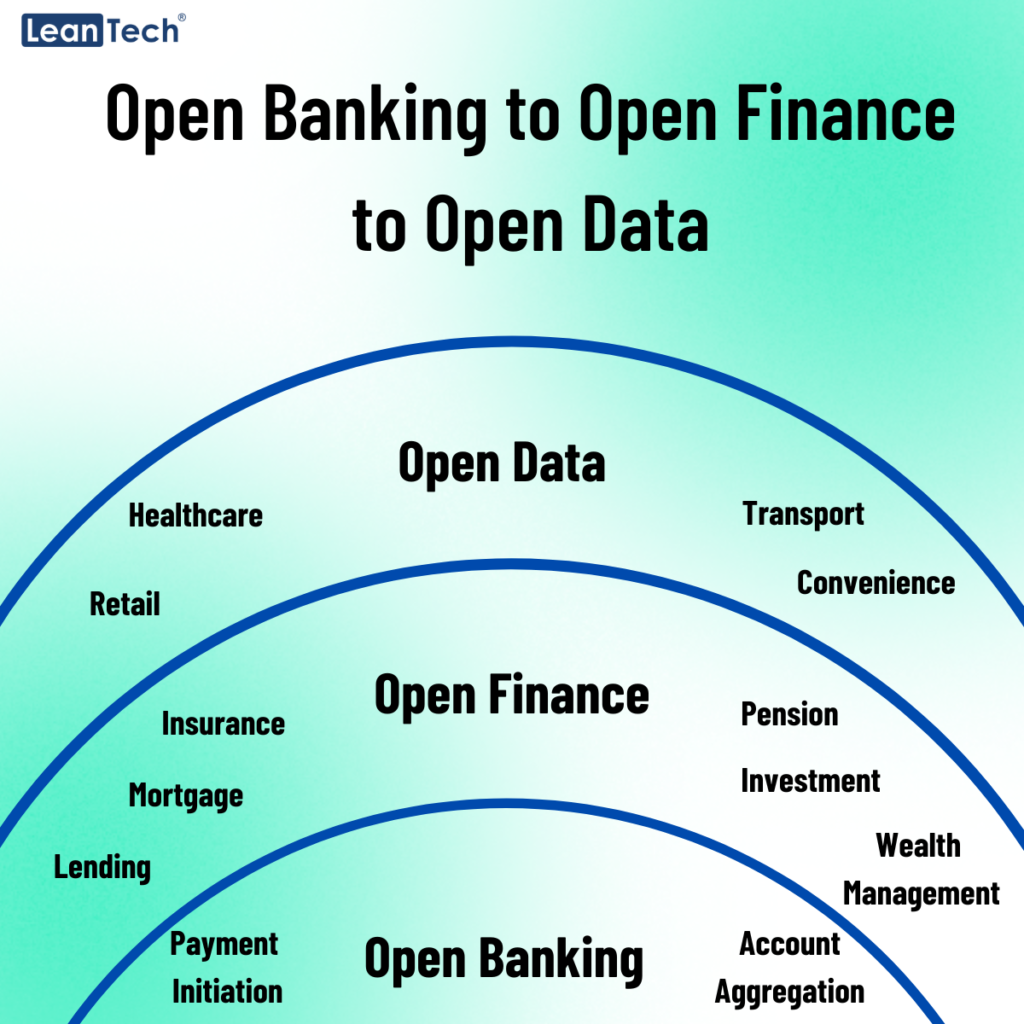

What is open banking vs open finance? Open banking focuses on payment and account data, while open finance extends to a consumer’s entire financial footprint, including pensions, insurance, and investments.